Understanding Letters of Credit in International Trade: A Dunrite Global Guide

Introduction: Securing Global Transactions

In the complex world of international trade, trust and security are paramount. When a buyer (importer) and a seller (exporter) are separated by thousands of miles and different legal systems, a mechanism is needed to ensure the seller gets paid and the buyer receives their goods. This is where the Letter of Credit (LC), also known as a Documentary Credit, becomes an indispensable tool.

A Letter of Credit is a contractual commitment by a bank, on behalf of a buyer, to pay a seller a specified sum of money, provided the seller presents the required shipping and commercial documents that comply with the terms of the LC. For businesses engaged in global commerce, understanding the nuances of LCs is crucial for mitigating risk and facilitating smooth transactions.

What is a Letter of Credit?

At its core, an LC is a bank's promise to pay. It shifts the payment obligation from the buyer to the buyer's bank, which is typically a more creditworthy entity. This mechanism is governed by the Uniform Customs and Practice for Documentary Credits (UCP 600), a set of rules published by the International Chamber of Commerce (ICC).

The Four Key Parties in an LC Transaction:

- Applicant (Buyer/Importer): The party who requests their bank to issue the LC.

- Issuing Bank: The bank that issues the LC on behalf of the applicant.

- Beneficiary (Seller/Exporter): The party who will receive payment under the LC.

- Advising Bank: A bank, usually in the seller's country, that authenticates the LC and advises it to the beneficiary.

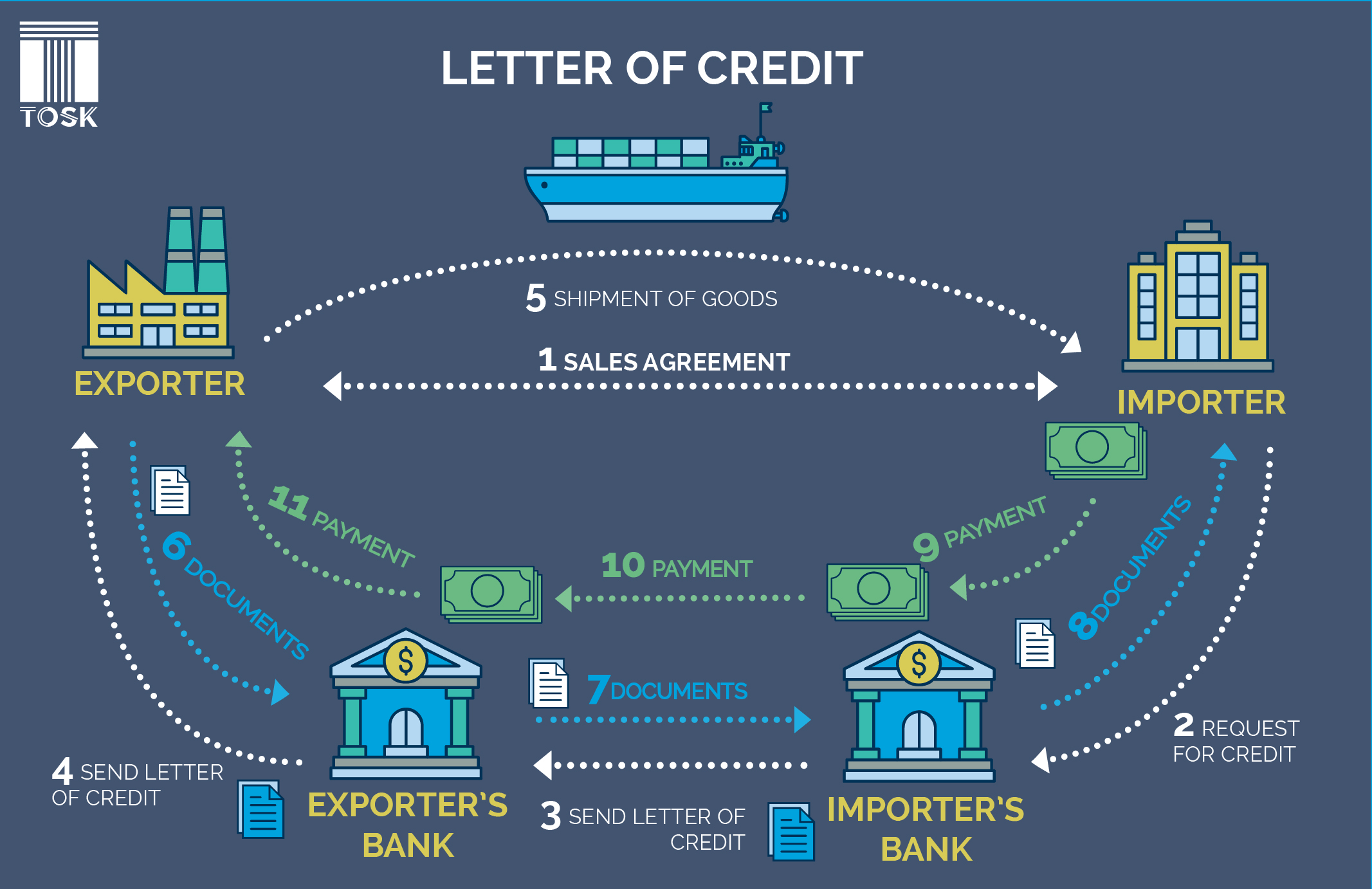

The LC Process in Brief:

- The buyer and seller agree on a sale, specifying that payment will be made via LC.

- The buyer applies to their bank (Issuing Bank) for an LC in favor of the seller.

- The Issuing Bank issues the LC and sends it to the Advising Bank.

- The Advising Bank verifies the LC's authenticity and forwards it to the seller.

- The seller ships the goods and prepares the required documents (e.g., bill of lading, commercial invoice, insurance certificate).

- The seller presents the documents to the Advising Bank (or a Nominated Bank).

- The banks examine the documents for strict compliance with the LC terms.

- If documents are compliant, the seller is paid, and the documents are forwarded to the Issuing Bank.

- The Issuing Bank releases the documents to the buyer, who can then take possession of the goods.

Key Types of Letters of Credit

The world of trade finance offers several variations of the LC, each suited for different risk profiles and transaction needs.

| Type of LC | Description | Primary Use Case |

|---|---|---|

| Commercial LC | The primary instrument for payment in a trade transaction. | Direct payment for goods in international sales. |

| Standby LC (SBLC) | A secondary payment mechanism; only drawn upon if the applicant defaults on their primary payment obligation. | Guaranteeing performance or financial obligations. |

| Irrevocable LC | Cannot be amended or canceled without the agreement of all parties. | Standard and most common type, offering maximum security to the seller. |

| Confirmed LC | A second bank (the Confirming Bank) adds its guarantee to the Issuing Bank's promise to pay. | Used when the seller is concerned about the creditworthiness or political risk of the Issuing Bank's country. |

| Revolving LC | Allows the LC amount to be automatically renewed or reinstated after it has been utilized. | Regular, ongoing shipments between the same buyer and seller. |

| Transferable LC | Allows the original beneficiary (often a middleman) to transfer all or part of the credit to a second beneficiary (the actual supplier). | Facilitating transactions involving intermediaries. |

Advantages of Using a Letter of Credit

For Dunrite Global's clients, the benefits of utilizing LCs in cross-border trade are significant:

- Security for the Exporter (Seller): The primary advantage is the assurance of payment. The risk of non-payment shifts from the buyer to the Issuing Bank.

- Security for the Importer (Buyer): Payment is only made when the seller provides documents that strictly conform to the LC's terms, ensuring the goods have been shipped as agreed.

- Facilitation of Trade: LCs enable trade between parties who may not know each other, bridging the trust gap inherent in global commerce.

- Access to Finance: An LC can often be used by the exporter as collateral to obtain pre-shipment or post-shipment financing.

Risks and Challenges

While highly secure, LCs are not without their complexities:

- Strict Compliance: The most common pitfall is documentary discrepancy. Banks deal in documents, not goods. If the documents presented by the seller do not strictly comply with the LC's terms, the bank can refuse payment.

- Cost: LCs involve various bank fees, including issuance, advising, and confirmation charges, which can add to the transaction cost.

- Complexity: The process is intricate and requires meticulous attention to detail and a thorough understanding of UCP 600.

Conclusion: The Foundation of Secure International Trade

The Letter of Credit remains a cornerstone of international trade finance. It is a powerful, globally recognized instrument that effectively manages the payment risks inherent in cross-border trade. For Dunrite Global's partners, mastering the use of LCs is not just about security; it's about opening up new markets and ensuring the seamless flow of global commerce.